Consolidating loans in Switzerland involves combining multiple debts into single financing. The goal is simple. You only pay one monthly installment, often lower. This solution can help when expenses multiply, interest rates are high, and budgeting becomes difficult to manage. In Switzerland, private credit can be used to restructure existing commitments, while respecting solvency and the framework of the LCC. In this guide, you will understand how this approach works, why it can reduce the monthly budget, and in which cases it can also lower the average rate.

Consolidation of loans in Switzerland: what exactly are we talking about?

Credit consolidation allows you to replace multiple loans with a single one. Specifically, a new loan is used to repay existing debts. Afterward, you are left with just one contract and one monthly payment.

In practice, we also talk about credit repurchase or refinancing. The terms are similar. However, the logic remains the same: reorganizing existing debts. In Switzerland, this operation often involves a personal loan used to restructure the budget.

Depending on the case, several types of debts may be involved:

- Credit cards

- small consumer loans

- money reserves

- some existing private credits

- sometimes other commitments, depending on feasibility

Not everything can always be grouped together. Approval depends on the application, income, and expenses. The establishment also analyzes solvency. He can consult the ZEK and check if the new financing remains affordable in the long term.

Why consolidating debts can relieve a monthly budget

The first advantage is simplicity. Instead of tracking multiple deadlines, you only manage one. This makes the budget more readable and stable.

Next, a lump sum payment often reduces monthly pressure. This point is very important when several payments fall on different dates. With a single fixed charge, it becomes easier to anticipate daily expenses.

Furthermore, the risk of forgetting decreases. Fewer deadlines mean fewer potential delays. This is useful for maintaining healthy management and avoiding additional fees.

Finally, this organization helps to regain control. In Switzerland, where the cost of living can strain the budget, a clearer repayment structure often brings real relief.

How is a lower monthly payment possible

A lower monthly payment is often possible thanks to a Repayment period longer. The total debt is spread over more months. The amount to be paid each month therefore decreases mechanically.

This brings immediate relief. On the other hand, you have to look at the whole operation. Paying less each month doesn't always mean paying less overall. If the term is extended significantly, the final cost can increase.

Credit consolidation therefore reduces the monthly charge, but it must be evaluated methodically. The right question isn't just: how much will I pay per month? You also need to ask: how much will I pay in total?

The trade-off to understand before diving in:

The immediate benefit is clear: the budget has more breathing room. However, this monthly comfort often comes with a trade-off. The duration can lengthen, sometimes significantly.

If the new rate isn't significantly better, the overall cost may remain high. That's why you need to compare the situation before and after. An attractive offer should improve the monthly payment without creating an imbalance. total cost.

In Switzerland, a relevant debt consolidation is not judged solely by the reduction in the monthly payment, but by the balance between the monthly charge, the repayment period, and the total cost of the operation.

When consolidating multiple small loans or credit cards becomes particularly advantageous

This solution often makes the most sense when debts are fragmented. Credit cards, cash reserves and certain small loans often show high rates. Separately, each amount seems manageable. Together, they weigh heavily.

The cumulative effect is sometimes underestimated. Several small monthly payments can end up exceeding a reasonable burden. Moreover, these scattered financings complicate the budget outlook.

Consolidating multiple loans allows for a more structured financing. In some cases, the average rate also decreases. This is especially true if the original debts are costly.

The typical cases are known:

- several Credit cards used in parallel

- small loans taken out at different times

- a cash reserve that has become difficult to bear

- A stacking of fragmented monthly payments

Does credit consolidation really allow you to pay less in interest?

Not automatically. Consolidating debts can lower your monthly payment without reducing the total cost. It all depends on the new interest rate, the term, and the debts being replaced.

The operation often becomes favorable when it replaces very expensive commitments with a personal loan to better conditions. This is common with certain Credit cards Or expensive little lines.

It is also important to distinguish between three concepts: the rate, the monthly payment, and the total cost. A lower monthly payment can be beneficial for the budget. However, if the term is extended too much, the advantage on interest can disappear.

In short, all conditions must be compared. The monthly payment alone is never enough to judge an offer.

Concrete example of credit consolidation in Switzerland

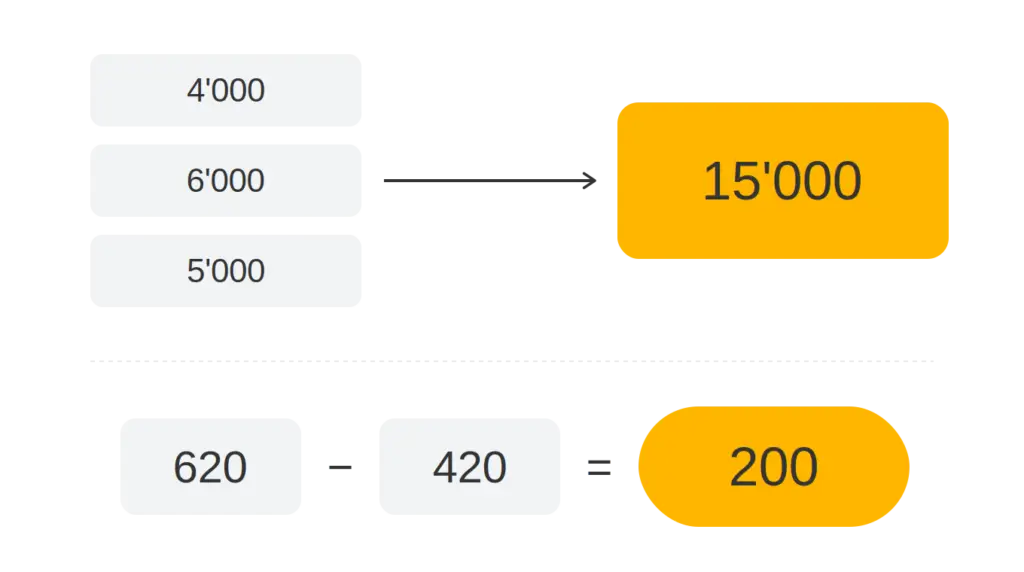

Let’s imagine a household with three debts: a credit card balance of 4,000 CHF, a small loan of 6,000 CHF, and a line of credit of 5,000 CHF. The total monthly payments amount to 620 CHF. The interest rates are high, and the household lacks financial clarity.

After grouping the credits, these amounts are replaced by A single private loan from 15,000 CHF. The new monthly payment is now 420 CHF. The monthly savings are therefore 200 CHF.

In return, the repayment period is extended. Previously, some debts could have been settled faster, but at the cost of high monthly pressure. Afterwards, the schedule becomes clearer and more stable.

According to the rate obtained, the total cost can be better, close, or sometimes higher. Therefore, the correct reading is: consolidation significantly improves the monthly budget here, but a simulation is needed to confirm if the total savings are real.

What requirements must be met in Switzerland to consolidate your loans?

The central condition remains solvency. The establishment analyzes revenue, fixed costs, and repayment capacity. In Switzerland, consumer credit is regulated. The lender must verify that the financing remains affordable.

Therefore, there is no guarantee of acceptance. A stable application improves your chances. Regular income, few payment incidents, and sound management are favorable points.

The regrouping must also serve a useful purpose. If it only postpones a problem without correcting the budget, it will be less relevant. The goal is not to add debt, but to organize it better.

In which cases is this solution relevant and in which cases is it less so?

This solution is often relevant if you have several expensive loans, with stable income but a tight budget. It is also suitable if you are looking a more manageable monthly payment and simpler management.

Conversely, it is less suitable if solvency is too fragile, if the duration becomes excessive, or if the interest rate spread is insufficient. One must also avoid a classic trap: consolidating one's debts and then taking out new loans.

Before deciding, a personalized analysis remains essential. It helps to see if grouping really helps or if it just shifts the difficulty.

The comparative table for credit consolidation:

| Comparison point | Before grouping | After grouping | To check |

|---|---|---|---|

| Number of debts | Multiple credits, cards, or reserves | One private credit | Which debts are actually eligible |

| Monthly payments | Multiple deadlines on different dates | A single monthly payment, often more readable | Maximum affordable amount according to budget |

| Monthly pressure | Often higher when debts add up | Can decrease if the duration is extended | Real impact on disposable income |

| Average rate | Often high with credit cards and small loans | Can be more advantageous depending on the case | Compare the new rate with the old ones |

| Repayment term | Varies depending on each debt | Often longer | Effect on total cost |

| Budget Management | More complex follow-up and risk of omission | Simplified budget and single deadline | Avoid taking on new debt |

| Conditions in Switzerland | Charges and commitments already in progress | Solvency analysis according to the LCC and possible consultation of the ZEK | Acceptance not guaranteed |

| Most relevant cases | Credit cards, small loans, cash reserve | Useful regrouping if income is stable and budget is under pressure | Simulation before decision |

How to know if a credit consolidation is truly advantageous?

To judge an offer, you actually need to compare five elements: the total monthly payment before and after, the rate of current debts, the rate of new financing, the repayment term, and the final total cost.

A healthy operation improves the monthly budget without excessively worsening the overall cost. That's why a Simulation Claire It is essential. It must present the figures in a simple and transparent way.

Serious support also helps to avoid misinterpretations. The right choice is not necessarily the lowest monthly payment. It's the one that remains balanced for your situation.

Our conclusion

Consolidating loans can offer several concrete advantages in Switzerland. It allows you to switch to one monthly payment, often lower, with simpler management. In some cases, it can also reduce the rate average, especially if the original debts are expensive.

However, this solution has its limits. The duration is often longer. The total cost must therefore be carefully checked. Furthermore, acceptance always depends on solvency. Before committing, a personalized simulation is the best way to know if credit consolidation is truly advantageous in your situation.